Introduction

Buying a home is one of the most significant financial decisions you’ll ever make. Whether you’re purchasing your first apartment, investing in a villa, or upgrading to a larger property, securing a home loan is often a critical part of the journey.

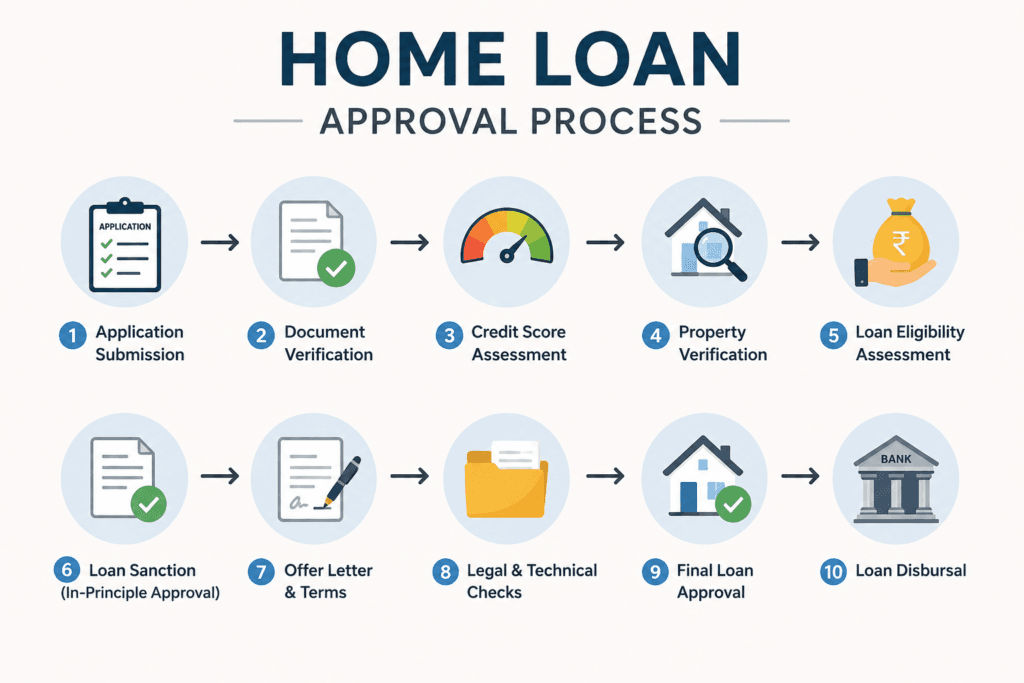

While lenders have made the application process faster and more digital, home loan approval still depends on several factors. Many applicants face delays or even rejections because they overlook basic eligibility requirements, documentation, credit score requirements, or property verification procedures.

A well-prepared home loan approval checklist can help you avoid common mistakes, improve your eligibility, and increase your chances of getting favourable loan terms.

In cities like Bengaluru, where real estate demand continues to grow due to expanding infrastructure, metro connectivity, and IT-driven employment opportunities, understanding the home loan approval process has become more important than ever.

This guide covers everything Indian homebuyers need to know before applying for a home loan, including eligibility criteria, required documents, property verification, RERA considerations, and expert tips to improve approval chances.

Table of Contents

- Why a Home Loan Approval Checklist Matters

- Quick Home Loan Approval Checklist

- Understanding Home Loan Eligibility

- Documents Required for Home Loan Approval

- Credit Score Requirements for Home Loans

- Property Verification Before Loan Approval

- RERA Compliance and Legal Verification

- Common Reasons Home Loan Applications Get Rejected

- Tips to Improve Home Loan Approval Chances

- Home Loan Approval Checklist for Investors

- Frequently Asked Questions

- Conclusion

Why a Home Loan Approval Checklist Matters

A home loan approval checklist helps borrowers prepare financially and legally before submitting an application.

Benefits of Following a Checklist

- Faster loan processing

- Reduced chances of rejection

- Better loan offers and interest rates

- Easier documentation process

- Improved financial planning

- Smooth property registration process

Many buyers focus only on finding the right property but neglect lender requirements. Preparing beforehand can save weeks of delays and prevent unnecessary stress.

Quick Home Loan Approval Checklist

Before Applying for a Home Loan, Ensure You Have:

✅ Credit score above 750

✅ Stable income source

✅ Minimum work experience as per lender requirements

✅ Low debt-to-income ratio

✅ Valid identity and address proof

✅ Income documents

✅ Bank statements

✅ Property documents

✅ RERA registration verification

✅ Legal property clearance

✅ Adequate down payment funds

Key Takeaway

Most lenders approve home loans faster when applicants have a strong credit profile, complete documentation, and invest in legally verified properties.

Understanding Home Loan Eligibility

Banks and housing finance companies evaluate several factors before approving a loan.

Income Stability

Your income is one of the biggest determinants of eligibility.

Lenders prefer applicants with:

- Stable employment

- Consistent salary growth

- Regular business income

- Predictable cash flow

Salaried Professionals

Typically need:

- 2–3 years of employment history

- Minimum tenure with current employer

- Salary credited to the bank account

Self-Employed Applicants

Usually require:

- Business continuity proof

- Income tax returns

- Audited financial statements

- GST records (if applicable)

Age Criteria

Most lenders accept applicants between:

| Criteria | Typical Range |

|---|---|

| Minimum Age | 21 Years |

| Maximum Age at Loan Maturity | 60–70 Years |

Younger applicants may qualify for longer repayment tenures, resulting in lower EMIs.

Debt-to-Income Ratio

Lenders assess your existing financial obligations.

Ideally:

- Total EMI commitments should not exceed 40–50% of monthly income.

- Lower liabilities improve approval chances.

Examples of liabilities include:

- Personal loans

- Car loans

- Credit card dues

- Education loans

Documents Required for Home Loan Approval

Documentation is a crucial part of the approval process.

Identity Proof

Accepted documents include:

- Aadhaar Card

- Passport

- PAN Card

- Driving License

- Voter ID

Address Proof

Commonly accepted documents:

- Aadhaar Card

- Utility bills

- Passport

- Rental agreement

Income Tax Department of India :

Salaried Applicants

- Last 3–6 months’ salary slips

- Form 16

- Income Tax Returns

- Bank statements

Self-Employed Applicants

- Income Tax Returns

- Profit and Loss Statement

- Balance Sheet

- GST Returns

- Business registration proof

Property Documents

Lenders carefully verify property ownership and legality.

Documents generally include:

- Sale Agreement

- Sale Deed

- Encumbrance Certificate

- Property Tax Receipts

- Approved Building Plan

- Occupancy Certificate (if applicable)

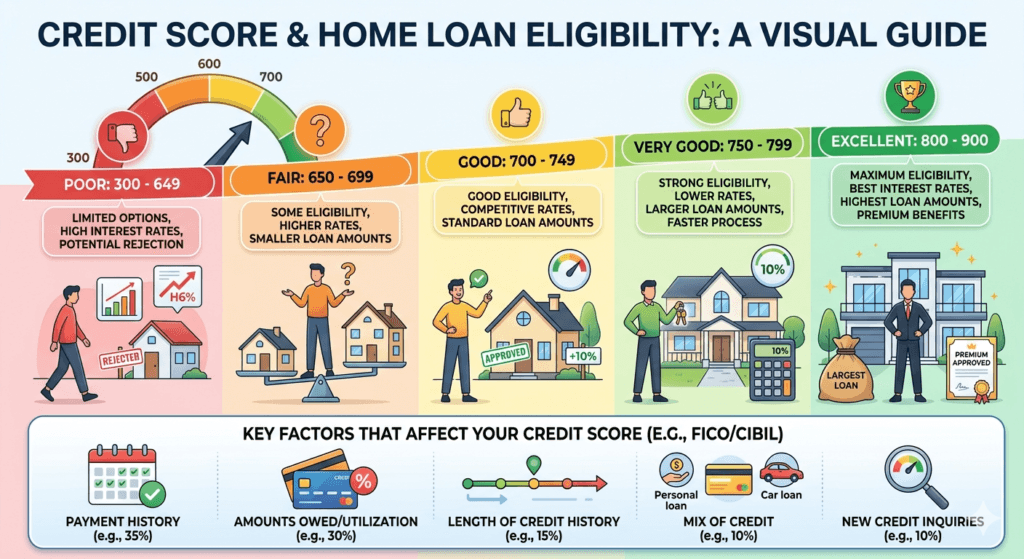

Credit Score Requirements for Home Loans

A credit score significantly influences loan approval and interest rates.

Recommended Credit Score Range

| Credit Score | Approval Chances |

|---|---|

| Above 800 | Excellent |

| 750–800 | Very Good |

| 700–749 | Good |

| 650–699 | Moderate |

| Below 650 | Difficult |

Check Your CIBIL Score

How to Improve Your Credit Score

1. Pay EMIs on Time

Consistent repayment demonstrates financial discipline.

2. Reduce Credit Utilisation

Keep credit card usage below 30% of the available limit.

3. Avoid Multiple Loan Applications

Frequent applications may negatively impact your credit profile.

4. Correct Credit Report Errors

Review your credit report periodically and rectify inaccuracies.

Property Verification Before Loan Approval

A lender evaluates not only the borrower but also the property being purchased.

Legal Verification

Ensure:

- Clear ownership title

- No legal disputes

- No pending litigation

- Proper registration history

Technical Verification

Banks inspect:

- Construction quality

- Property valuation

- Building approval status

- Compliance with local regulations

RERA Verification

For under-construction properties, verify registration through the Karnataka RERA portal.

Why RERA Matters

RERA protects homebuyers by ensuring:

- Project transparency

- Timely completion

- Proper disclosures

- Legal accountability

Purchasing a RERA-registered property reduces risk and improves lender confidence.

Common Reasons Home Loan Applications Get Rejected

Understanding rejection factors helps avoid costly mistakes.

Low Credit Score

Poor repayment history often leads to rejection.

Insufficient Income

Income may not support the requested loan amount.

High Existing Debt

Excessive liabilities increase lending risk.

Incomplete Documentation

Missing paperwork can delay or halt approval.

Property-Related Issues

Examples include:

- Unclear title ownership

- Unauthorized construction

- Missing approvals

- RERA non-compliance

Tips to Improve Home Loan Approval Chances

Increase Down Payment

A larger down payment lowers lender risk.

Benefits include:

- Lower loan amount

- Better interest rates

- Reduced EMI burden

Maintain Financial Discipline

Before applying:

- Avoid unnecessary loans

- Pay bills on time

- Clear outstanding dues

Choose the Right Loan Amount

Borrow within your repayment capacity.

Do not rely solely on the maximum amount offered by lenders.

Apply Jointly

A co-applicant can improve eligibility.

Common co-applicants include:

- Spouse

- Parents

- Earning family members

Compare Multiple Lenders

Evaluate:

- Interest rates

- Processing fees

- Prepayment charges

- Loan tenure options

A lower interest rate can save several lakhs over the loan tenure.

Home Loan Approval Checklist for Property Investors

Investors should assess additional factors beyond loan approval.

Rental Yield Potential

Estimate:

- Expected monthly rent

- Vacancy rates

- Maintenance costs

Infrastructure Growth

Properties near major developments often appreciate faster.

In Bengaluru, infrastructure drivers include:

- Namma Metro expansion

- Peripheral Ring Road

- Satellite Town Ring Road

- IT corridor development

- Airport connectivity projects

Future Appreciation Potential

Look for:

- Emerging micro-markets

- Planned commercial hubs

- Employment growth zones

- Educational and healthcare infrastructure

Strategic property selection can improve both rental returns and long-term capital appreciation.

Home Loan Approval Checklist Summary

| Checklist Item | Importance |

|---|---|

| Credit Score Above 750 | High |

| Stable Income | High |

| Complete Documentation | High |

| RERA Verification | High |

| Property Legal Clearance | High |

| Adequate Down Payment | Medium |

| Low Existing Debt | High |

| Proper Financial Planning | High |

Frequently Asked Questions

1. What credit score is required for a home loan in India?

Most lenders prefer a credit score of 750 or above for faster approvals and better interest rates. Some lenders may approve loans with lower scores, but terms may be less favourable.

2. How much down payment is required for a home loan?

Typically, banks finance 75%–90% of the property’s value. Buyers usually need to contribute 10%–25% as a down payment.

3. Can a home loan be approved for an under-construction property?

Yes. However, lenders usually prefer RERA-registered projects with proper approvals and clear documentation.

4. How long does home loan approval take?

Depending on documentation quality and lender processes, approval may take anywhere from a few days to several weeks.

5. Does property verification affect home loan approval?

Absolutely. Even if the applicant qualifies financially, lenders may reject the loan if the property has legal, technical, or regulatory issues.

Conclusion

Securing a home loan is not just about meeting income requirements. Lenders evaluate your financial profile, repayment capacity, documentation, creditworthiness, and the legal status of the property.

Following a comprehensive home loan approval checklist can significantly improve your chances of approval while helping you secure better loan terms and avoid costly mistakes.

For homebuyers and investors in Bengaluru, combining financial readiness with proper property verification and RERA compliance is the smartest way to make a confident real estate investment.

Whether you’re buying your first home, upgrading to a larger property, or investing for long-term appreciation, careful planning today can lead to greater financial stability tomorrow.

Need Expert Property Guidance?

Navigating home loans, property verification, RERA compliance, and investment decisions can be overwhelming. The experienced team at Sampoorna Realty Group can help you identify the right property, evaluate investment opportunities, and make informed real estate decisions.

Contact Sampoorna Realty Group today for trusted guidance on buying, investing, and financing your dream property in Bengaluru.